海外之声 | 日本央行货币政策框架的最新调整

导读

本文阐述了日本央行货币政策框架的最新调整,特别是其停止量化和定性宽松货币政策(QQE)与收益率曲线控制(YCC),并引入全新政策框架的决策。此前,日本央行通过调控短期与长期利率和为10年期日本政府债券(JGB)利率设定清晰目标以稳定经济。然而,在今年的3月,日本央行果断调整策略,设定了新的短期利率目标,并取消了原有的10年期日本国债利率目标。

在资产购买方面,日本央行依旧保持原有的日本国债购买速度,并在长期利率显著上升时增加购买量以维持市场稳定。此外,央行已停止了对与股票相关的交易型开放式指数基金(ETFs)和日本房地产投资信托(J-REITs)的购买,并计划在未来一年内逐步将商业票据和公司债券的购买量削减至零。至于日本国债购买的缩减安排,目前尚待进一步明确。

目前,日本央行的货币政策主要聚焦于通过调整短期利率来实现2%的可持续通胀率目标。这一政策调整反映了全球及国内环境对通胀前景的积极预期。近期的通胀动态,包括全球通胀的直接影响、对工资和价格的连锁反应以及通胀预期的增强,均为此次政策调整提供了有力支撑。考虑到能源价格、服务价格以及工资趋势等多重因素,本文还探讨了准确评估潜在通胀的复杂性。尽管通胀率近期有所上升,但基本通胀率尚未达到2%的目标。对产品和服务价格水平预期的深入分析,揭示了企业定价行为在克服根深蒂固的通胀预期中所面临的挑战。

在强劲的薪资增长与稳定的国内需求双重驱动下,市场对实现通胀目标的信心不断增强。展望未来,日本央行计划继续维持宽松的金融环境,同时密切关注并审慎评估近期政策变动对经济和通胀的潜在影响,必要时央行将灵活调整政策,并特别关注中性利率对未来政策决策的影响。

作者丨上田和夫(日本银行行长)

On the Recent Changes in the Bank of Japan’s Monetary Policy Framework

UEDA Kazuo, Governor of the Bank of Japan

Remakrs at the Peterson Institute for International Economics

April 19, 2024

In the March monetary policy meeting, taking into consideration the improving inflation outlook, the Bank of Japan (BOJ) opted to discontinue the policy framework known as Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control (YCC), which had been in effect since 2013 with revisions made after 2016. In its place, we introduced a new framework. First, I will give a brief outline of the changes made, followed by an explanation of the background behind these adjustments.

展开全文

Regarding interest rates, under YCC, we controlled both short- and long-term interest rates. The short-term policy rate -- the interest rate the BOJ pays on the policy component of excess reserves -- stood at -0.1% as of early March this year. Meanwhile, the target for the 10-year JGB rate was set at around 0%, with a permitted fluctuation range around the target capped at 1.0%.

On March 19, we decided to establish a new short-term interest rate target, now defined as the uncollateralized overnight call rate, set between 0 and 0.1%. The target for the 10-year JGB rate has been removed.

As for asset purchases, we will maintain our acquisition of JGBs at a pace similar to before, thereby keeping the amount of JGBs held by the BOJ relatively stable for the time being. However, we remain prepared to respond swiftly to any rapid increase in long-term interest rates by increasing our purchases of JGBs. Other than these, the determination of long-term interest rates is left to the market.

We have ended the acquisition of equity-linked ETFs and J-REITs, gradually reducing purchases of CP and corporate bonds to zero within approximately one year.

We will begin to reduce JGB purchases at an unspecified point in the future. However, the extent of this reduction remains undetermined. We will need to take time to consider what to do with the ETFs we hold.

Given these changes, the primary tool of our monetary policy has become control of the short-term interest rate, with the policy target continuing to be the attainment of 2% inflation in a sustainable manner. Based on our current economic and inflation outlook, we anticipate accommodative financial conditions to prevail for the time being.

Turning to the background for this policy change, let me discuss how the inflation outlook has improved. Our previous monetary policy framework involved the commitment to maintain YCC until a sustainable 2% inflation target was within reach. In other words, we promised to persist with YCC until we were sufficiently confident that inflation would soon reach 2% on a sustained basis.

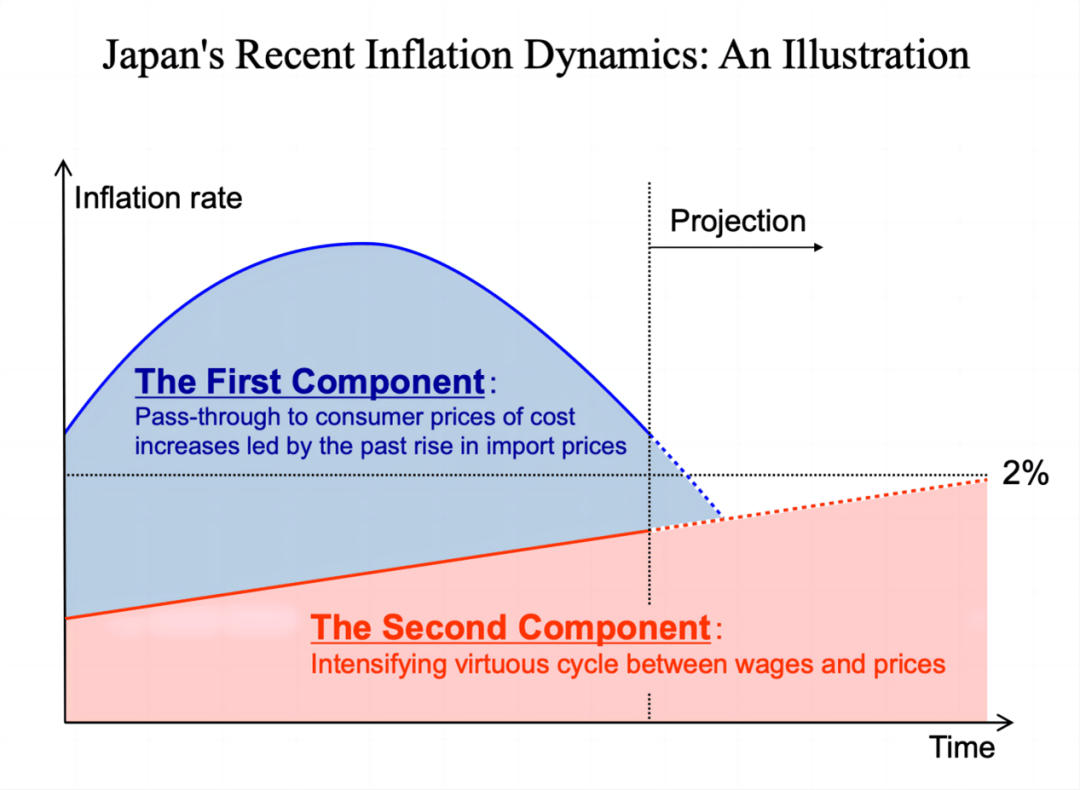

Figure 1 provides a simple illustration of Japan’s inflation dynamics. Recent inflation, which has exceeded 2% for nearly two years, consists of two main components: the direct (first-round) effects of global inflation during 2021-23, and second-round effects, which represent the spillover to wages and, subsequently, to prices. The latter component has been accompanied by rising inflation expectations. The first component, deemed transitory, has been diminishing since late last year. The second component, often referred to as underlying inflation, is more enduring.

This broader inflation picture mirrors that of many other countries. A notable distinction between Japan and others lies in Japan entering the pandemic era with nearly zero inflation, while others were already at around 2%. Consequently, the BOJ has endeavored to cultivate the second component by maintaining an ultra-easy monetary policy, contrasting with the efforts of other central banks to contain it.

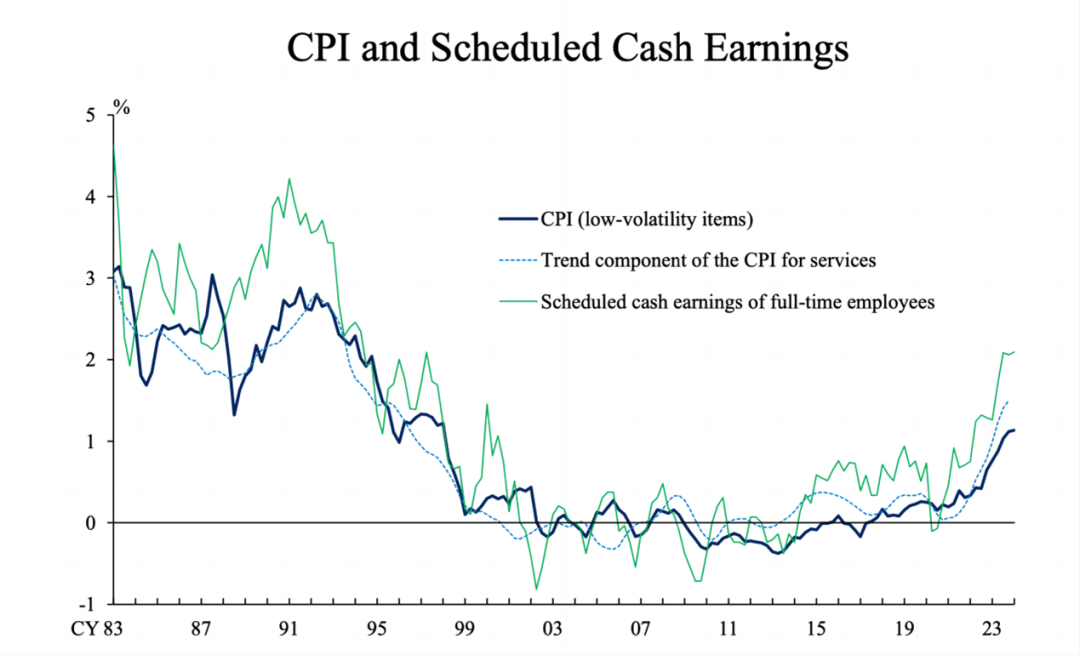

Estimating underlying inflation accurately is particularly challenging because of the varied forms temporary inflation changes can assume. These changes may manifest as alterations in energy and fresh food prices or may extend to impacts on transportation costs and dining-out expenses. Figure 2 shows some easily available inflation variables that have some bearing on underlying inflation. One is the inflation of those items whose prices do not change frequently. Another is an estimated trend component of inflation of service prices. Both have been rising recently but need to rise slightly more to get to 2%. We use more sophisticated statistical techniques to estimate underlying inflation in a variety of ways, yielding consistent conclusions. The figure also includes the rate of change in regular wages of full-time workers. The broad picture is the same. Please note that wages need to rise faster than 2% to be consistent with prices rising at 2% in the presence of positive productivity gains.

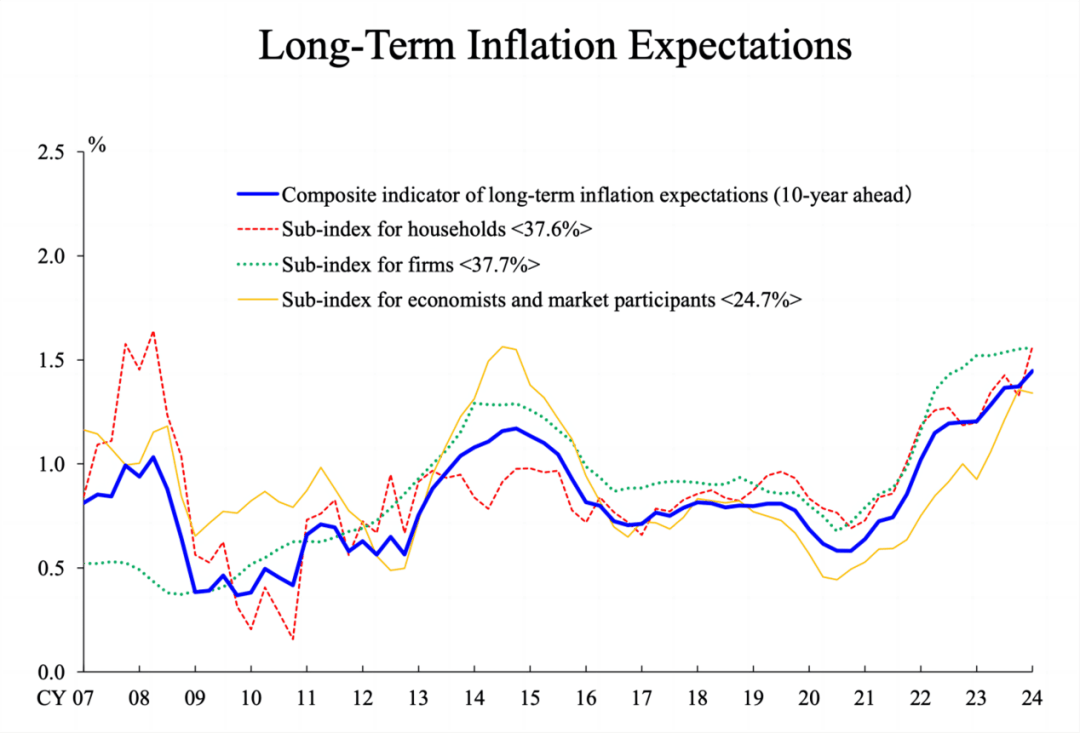

Medium- to long-term inflation expectations closely track underlying inflation trends. Figure 3 shows the weighted average of such expectations, indicating a rising trend but remaining below 2%.

Let me try to add some color to this outline sketch. People often ask why inflation in Japan got stuck at around zero despite the heavy dose of unconventional monetary policy measures over three decades. One possible answer is that inflation expectations became so entrenched at around zero that economic agents changed their behavior to make zero inflation more enduring.

Theoretically, easy money could have produced higher inflation; in reality, it did not. This may be a multiple equilibrium type situation where easy money is consistent with either zero or higher inflation. The driver of equilibrium multiplicity seems to have been the strategic pricing behavior of firms in the economy. When firms believe their peers will not raise prices, they think it is best to keep their own prices and wages unchanged, even in the face of small changes in costs or demand, making overall inflation or inflation expectations more entrenched at around zero. An economy in this situation needs a large shock to move from one equilibrium to the other.

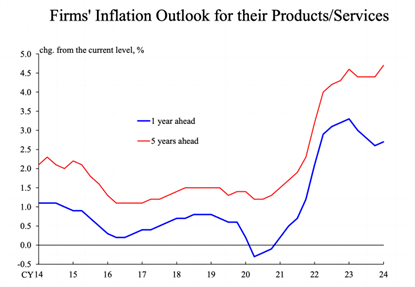

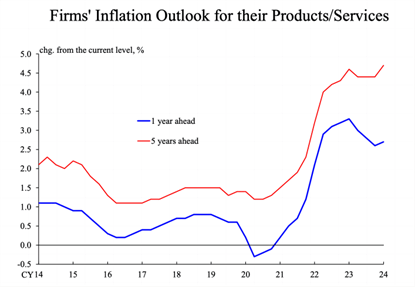

Figure 4 shows Japanese firms' expectations of the price level of their products/services, not the general price level, at both one- and five-year horizons sourced from our Tankan survey. These presumably reflect firms' expectations about what their competitors in the same industry are likely to do with their prices. While one-year expectations peaked in late 2023 before declining, five-year expectations have continued to rise. Apparently, the global inflation experienced during 2021-23 has created a lasting change in firms' pricing behavior, perhaps providing a catalyst for movement from the zero to a positive inflation equilibrium.

Returning to the explanation of the recent BOJ policy change, alongside these observations on underlying inflation and inflation expectations, robust initial wage settlements from spring wage negotiations have emerged since mid-March. Figure 5 shows these settlements to be at their highest level in three decades, while evidence of a moderate upward trend in domestic demand for goods and services has further bolstered our confidence. Based on these factors, we concluded in the March Monetary Policy Meeting that the probability of achieving a stable 2% inflation rate has increased enough to justify the outlined policy normalization.

What lies ahead? Given that underlying inflation is still somewhat below 2%, we need an easy financial environment. Figures 2-4 suggest that long-term inflation expectations are above 1%, perhaps closer to 1.5%. Estimates of the neutral interest rate vary widely. However, unless the real neutral rate is deeply negative, the nominal policy rate of 0.1% implies a fairly accommodative financial environment. We will proceed cautiously, initially assessing the impact of the recent policy changes on the economy and inflation, and then considering further adjustments as deemed appropriate, perhaps extracting insights on the neutral rate along the way.

编译:周杼樾

监制:崔洁

来源|日本央行

版面编辑|刘书廷

责任编辑|李锦璇、蒋旭

主编|朱霜霜

近期热文

周末读史丨《黄达传略》:坎坷少年 (1925~1950)

DEPA数据开放共享规则:框架分析与影响对比

吴晓求:资本市场应在IPO阶段确立正确理念 并尽快完善投资者救济和赔偿制度

张景安:金融促进科技创新,加快发展新质生产力

朱太辉:大中小企业数字化转型的“融合蝶变之路”

评论